I can already see start to creep into every private markets pitch over the next couple of quarters. The idea is that because public markets are a top-heavy AI casino, you should hide out in the private markets for safety. They’re insulting your intelligence.

They want you to believe that volatility is the risk in and of itself, and the real value is being created behind closed doors where the mark-to-market is non-existent. But as an investor (or LP) one of your biggest risks isn’t the movement in price. It’s the risk of you never having a chance to generate the returns you were hoping for. Look at the actual dispersion of returns; it’s the real K-shaped economy.

In the public markets you’re forced to deal with the quirk of concentration at the top of the index. But at least you have the option to buy those winners. In private equity, you’re often just buying the median. And the median is starting to look like dead money.

The Exclusive Cap Table

The Mag 7 has been discussed ad nauseum as some sort of bug of the public markets. But in private markets, concentration is the entire game; you just don’t have the liquidity to chase it. The foundation model companies raised roughly $211B last year. But the capital is moving into a microscopic funnel.

Just five companies -OpenAI, Anthropic, xAI, Scale AI, and Project Prometheus- captured $84 billion, or 20% of all global venture funding. Judging by the cap tables venture capital and private equity haven’t been democratized just yet. They are dominated by hyperscalers and a tiny God-tier list of VCs. If you aren’t an LP in the top 1% of funds, you aren’t exposed to the disruption. You’re paying 2% just to be a spectator.

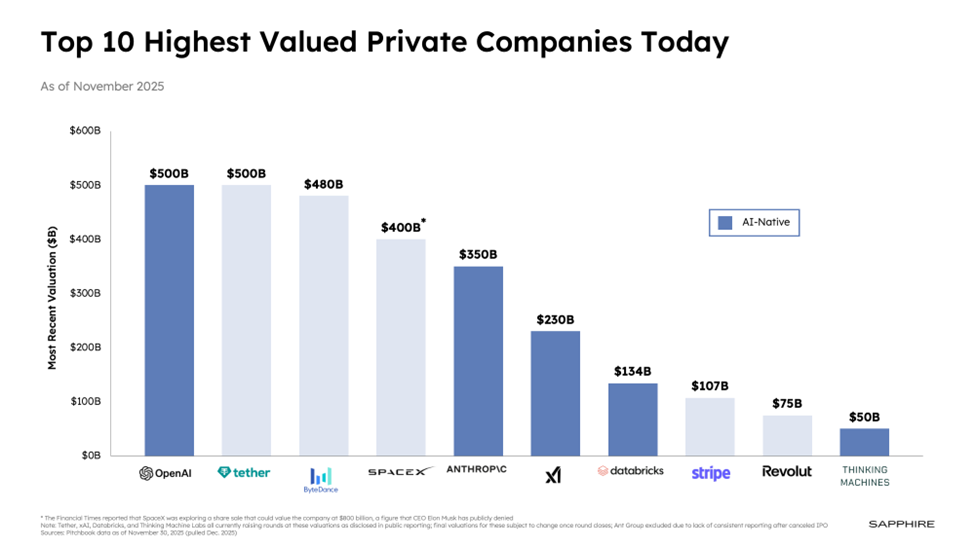

Check out this chart from Sapphire. The top 10 private software companies -names like OpenAI, Anthropic, and Databricks- are now worth $1.5 trillion. That is nearly 1/5th of the total public software universe!

While the public market is valued at a median of 4.2x NTM revenue, the private market winners are trading at a median ARR multiple of 25.9x.[1] You are paying a massive premium for the privilege of being private, yet access remains incredibly narrow.

The 95/5 Problem

The return dispersion in private markets isn’t a gap; it’s a chasm. Cambridge Associates’ data has long shown that ~5% of venture funds account for ~95% of the industry’s total returns. Let that sink in. This shouldn’t be a surprise to anybody who’s been paying attention to the industry longer than in the post-Covid era. Marc Andreessen has (in?)famously said that there are only about 15 companies a year that matter to VCs. And his job is to get in those deals. It’s the nature of power-law.

While the top-decile funds are feasting on the few winners, the median fund is struggling.

This is the moment where we have to be honest: the growth that was forecast in 2021 simply didn’t materialize. These assets were already worth a lot less than what people paid for them. Now, AI is the cherry on top. It’s the final, existential blow to business models that were already failing to grow into their valuations. If you’re stuck in a median fund, you’re likely holding a portfolio of mid-market (emphasis on mid) SaaS companies that are currently being dismantled by agentic AI tools while you wait for a 2021-era exit that is never coming.

The Index Mirage

For all the scrutiny passive indexes have gotten over the years—with some even comparing them to a form of Marxist capital allocation—the reality is that if you purely owned the index, you’re largely not experiencing the pain under the surface right now. Everyone deep in tech or finance is in full freakout mode over the pace of AI progress we’ve seen over the past two months. If you just owned the market, you barely notice the carnage.

Not to mention, your returns have ranked consistently in the top quartile. But that’s neither here nor there.

Liquidity as a Weapon

The volatility that we’ve seen over the last 6-7 months across software stocks, and now broadening out to other industries, is an example of liquidity at work. Whether rational or not, when the market even considered believing that a legacy player was being rendered obsolete by agentic AI, the market moved with a cold, efficient ruthlessness.

Prices fell and capital rotated into the winners. That’s the beauty of a liquid tape. You see the shift, and you can act.

But if you’re an LP in a private fund, you are effectively tied to the mast while the storm rolls in. You are holding a slice of the 16,000-plus companies globally that have been sitting in PE portfolios for over four years, the highest aging inventory on record by the way.

What is somewhat underappreciated at the moment is that if there is a systemic issue with private credit, the implied equity value for much of the PE space is in a bigger bind than the credit might be. If the credit is impaired even slightly, the equity is effectively wiped out.

You’re paying 2-and-20 for the privilege of illiquidity while your underlying assets are being systematically dismantled by a Python script generated by a LLM that was prompted by a person who doesn’t know what a token is.

The GP tells you volatility is low because they haven’t marked the asset down yet, but that’s just an accounting fiction. The value is gone. You just aren’t allowed to leave the building yet.

The Bottom Line

Don’t let a capital raiser convince you that missing the volatility is the same as missing the risk. The safety of private markets right now is an accounting trick. I’d rather take the volatility of a liquid market where I can move my feet and hunt for mispriced winners than the stability of a private portfolio that’s effectively a burning building with the doors locked from the outside.

[1] Data provided by Sapphire.

IMPORTANT LEGAL DISCLOSURES

CURRENT MARKET DATA IS AS OF 02/23/2025. OPINIONS AND PREDICTIONS ARE AS OF 02/23/2025 AND ARE SUBJECT TO CHANGE AT ANY TIME BASED ON MARKET AND OTHER CONDITIONS. NO PREDICTIONS OR FORECASTS CAN BE GUARANTEED. INFORMATION CONTAINED HEREIN HAS BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE BUT IS NOT GUARANTEED.

THIS PRESENTATION (THE “PRESENTATION”) HAS BEEN PREPARED SOLELY FOR INFORMATION PURPOSES AND IS NOT INTENDED TO BE AN OFFER OR SOLICITATION AND IS BEING FURNISHED SOLELY FOR USE BY CLIENTS AND PROSPECTIVE CLIENTS IN CONSIDERING GFG CAPITAL, LLC (“GFG CAPITAL” OR THE “COMPANY”) AS THEIR INVESTMENT ADVISER. DO NOT USE THE FOREGOING AS THE SOLE BASIS OF INVESTMENT DECISIONS. ALL SOURCES DEEMED RELIABLE HOWEVER GFG CAPITAL ASSUMES NO RESPONSIBILITY FOR ANY INACCURACIES. THE OPINIONS CONTAINED HEREIN ARE NOT RECOMMENDATIONS.

THIS MATERIAL DOES NOT CONSTITUTE A RECOMMENDATION TO BUY OR SELL ANY SPECIFIC SECURITY, PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. INVESTING INVOLVES RISK, INCLUDING THE POSSIBLE LOSS OF A PRINCIPAL INVESTMENT.

INDEX PERFORMANCE IS PRESENTED FOR ILLUSTRATIVE PURPOSES ONLY. DIRECT INVESTMENT CANNOT BE MADE INTO AN INDEX. INVESTMENT IN EQUITIES INVOLVES MORE RISK THAN OTHER SECURITIES AND MAY HAVE THE POTENTIAL FOR HIGHER RETURNS AND GREATER LOSSES. BONDS HAVE INTEREST RATE RISK AND CREDIT RISK. AS INTEREST RATES RISE, EXISTING BOND PRICES FALL AND CAN CAUSE THE VALUE OF AN INVESTMENT TO DECLINE. CHANGES IN INTEREST RATES GENERALLY HAVE A GREATER EFFECT ON BONDS WITH LONGER MATURITIES THAN ON THOSE WITH SHORTER MATURITIES. CREDIT RISK REFERES TO THE POSSIBLITY THAT THE ISSUER OF THE BOND WILL NOT BE ABLE TO MAKE PRINCIPAL AND/OR INTEREST PAYMENTS.

THE INFORMATION CONTAINED HEREIN HAS BEEN PREPARED TO ASSIST INTERESTED PARTIES IN MAKING THEIR OWN EVALUATION OF GFG CAPITAL AND DOES NOT PURPORT TO CONTAIN ALL OF THE INFORMATION THAT A PROSPECTIVE CLIENT MAY DESIRE. IN ALL CASES, INTERESTED PARTIES SHOULD CONDUCT THEIR OWN INVESTIGATION AND ANALYSIS OF GFG CAPITAL AND THE DATA SET FORTH IN THIS PRESENTATION. FOR A FULL DESCRIPTION OF GFG CAPITAL’S ADVISORY SERVICES AND FEES, PLEASE REFER TO OUR FORM ADV PART 2 DISCLOSURE BROCHURE AVAILABLE BY REQUEST OR AT THE FOLLOWING WEBSITE: HTTP://WWW.ADVISERINFO.SEC.GOV/.

ALL COMMUNICATIONS, INQUIRIES AND REQUESTS FOR INFORMATION RELATING TO THIS PRESENTATION SHOULD BE ADDRESSED TO GFG CAPITAL AT 305-810-6500.