The Death of Simple Physics – In classical mechanics, the “Two-Body Problem”—predicting the movement of two objects interacting with each other, like the Earth and the Moon—is mathematically solvable. It is predictable. It is stable.

For the last three years, investors have enjoyed a financial version of the Two-Body Problem. To make money, you only had to solve for two variables: Inflation and Nvidia.

If inflation was falling, you bought. If Nvidia was rising, you bought. The rest of the S&P 500 was largely irrelevant “dark matter,” floating passively in the background while the Hyperscalers exerted all the gravitational pull. It was a period of historic concentration, but also historic simplicity.

As we enter 2026, the physics of the market are changing. We are moving from a predictable Two-Body system to a chaotic “493-Body Problem.”

The gravitational center of the market is shifting. The correlation between the mega-caps and the median stock is breaking down. The “Easy Beta” trade—where you could simply buy the index and go to sleep—is being replaced by a regime of high dispersion, where the returns will be generated by the 493 companies that have spent the last few years in the shadows.

This transition is confusing the consensus. Investors, addicted to the clarity of the last cycle, have fallen into what we call “The Binary Trap.” They are frantically looking for a binary outcome: Boom or Bust? AI Utopia or Hard Landing? Melt-up or Meltdown?

But reality rarely plays out at the extremes. We believe 2026 will be defined not by a binary explosion, but by a “Delicate Balance.” We are entering a classic “Recovery Year”, which is a period roughly 18 months after a bear market bottom (Liberation Day). History suggests these years are deceptively strong, often producing double-digit returns, but the composition of those returns flips upside down.

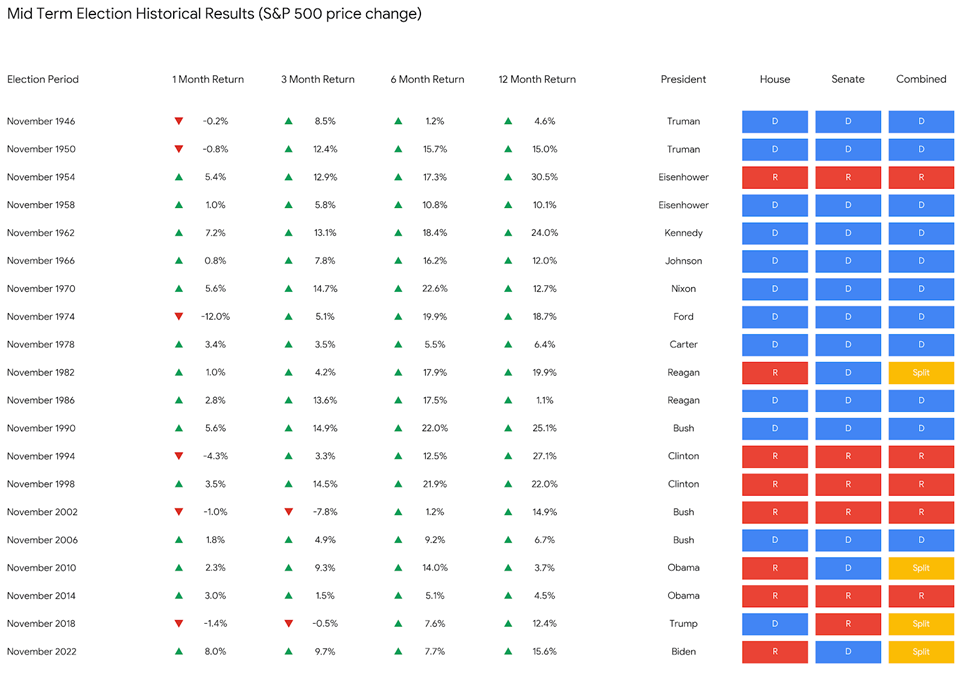

The Midterm Anomaly: The Consistency of the Incumbent

The first variable in our new equation is the political calendar. 2026 is a Midterm Election year, and markets famously hate uncertainty.

The standard bearish narrative for 2026 relies heavily on “Midterm Seasonality.” The consensus view is that the first half of a midterm year is a graveyard for momentum—volatility spikes, liquidity thins, and investors de-risk until the votes are counted in November. The “Binary Trap” thinkers will likely interpret any early-year chop as the start of a recession.

But this generic view misses a crucial distinction: Not all midterms are created equal. The party in the White House matters.

When you filter the historical data for Midterm years where a Republican is in the Oval Office, the volatility narrative completely collapses. In fact, the consistency is startling.

In generic midterm years, roughly 3 of the 12 months skew negative on a consistency basis. But when a Republican holds the presidency, there isn’t a single month where the return positivity rate drops below 50%. Every single month skews more positive than negative.

Entering the new year, prediction markets seem to point to a split government between a Democratic lead House and Republican controlled Senate. If this ends up being the case, in the 4 instances of a split government in past cycles; twelve months following the election markets have been positive 100% of the time with an average return of 12.5%.

The Takeaway: The market is likely overestimating the political risk premium. While the headlines will focus on the legislative battles for the House and Senate, the underlying market mechanism under this specific political configuration has historically been a steady, relentless grind higher. The “uncertainty” that usually caps gains in H1 may simply fail to materialize. Investors waiting for the “Midterm Dip” to deploy capital might find themselves chasing a market that refuses to correct.

[1] Chart generated by GFG Capital. Data provided by Bloomberg database.

The Great Rotation: “PTSD” in the Real Economy

If 2025 was the year of Concentration, 2026 will be the year of Capital Recycling.

We are witnessing a valuation gap that is becoming mathematically unsustainable. The Hyperscalers are priced for perfection, while the “Old Economy” cyclicals are trading at discounts reminiscent of the 2020 lows. But the catalyst for rotation isn’t just valuation; it is a fundamental shift in corporate behavior known as “Post-Traumatic Supply Disorder” (PTSD).

This is a concept we’ve borrowed from sector specialists to explain a strange phenomenon in the industrial base. In previous cycles, when demand rose, cyclical companies (Energy, Industrials, Materials) would immediately rush to build new factories, drill new wells, and flood the market with supply, eventually crashing their own margins.

Not this time.

The management teams of the S&P 493 have been traumatized by the oversupply disasters of the 2010s (Shale) and the post-COVID whiplash (Inventory Gluts). As a result, they have effectively gone on a “Capital Strike.” Even as demand recovers, they are refusing to add capacity.

- The Energy CEO is prioritizing dividends over drilling.

- The Memory Chip Manufacturer is prioritizing margin over market share.

- The Airline is prioritizing pricing power over route expansion.

This “PTSD” creates a structural floor under margins. It means that for the first time in decades, an increase in demand will flow directly to the bottom line rather than being diluted by new supply.

This supports our broader earnings thesis: We are moving from “Narrow Leadership” to “Broad Participation.” Consensus data for 2026 shows that 59 of the 62 major industry groups are projected to show positive earnings growth. The “Profit Boom” is leaving Silicon Valley and entering the Rust Belt.

AI Phase 2: From the Cloud to the Edge

Does this mean the AI trade is dead? Absolutely not. But the location of the trade is moving.

Phase 1 of the AI revolution (2023-2025) was about Infrastructure. It was about Hyperscalers building the “Cloud”, i.e. the massive data centers, the H100 clusters, and the utility grid connections. This trade has been incredibly profitable, but it is now crowded and priced for a “perfect” execution ramp.

Phase 2 (2026 and beyond) will be about Inference. It is about taking the intelligence out of the data center and putting it into the device in your pocket.

There is a physical limit to how much “Cloud AI” we can afford. Running a query on a massive server farm is expensive, energy-intensive, and suffers from latency. If the “Agentic Future” (where AI acts as your personal assistant) is going to happen, it cannot happen in the cloud. It must happen on the device.

This creates a new set of winners in the semiconductor supply chain. The bottleneck is shifting from the GPU (the brain of the data center) to the NPU (Neural Processing Unit) and High-Bandwidth Memory on the smartphone.

We are positioning for an “Inference Super-Cycle” in consumer electronics. The hardware requirements to run a decent LLM locally on a phone are massive—requiring a step-change in DRAM and logic. This benefits the Memory manufacturers (who are also practicing “PTSD” supply discipline) and the IP owners of edge architecture.

The Hyperscalers built the factory. Now we are buying the delivery trucks.

The “Hard” Pivot: Atoms and Tokens

Finally, solving the 493-Body Problem requires a re-evaluation of the defensive side of the ledger.

For forty years, the 60/40 portfolio relied on a simple negative correlation: US Treasuries were the ultimate “Risk-Off” asset. When stocks fell, bonds rose. They were the perfect hedge. But as we move deeper into 2026, investors should consider whether that correlation is fraying.

With the fiscal deficit running near 6% of GDP in a non-recessionary environment, the risk of “Fiscal Dominance” is rising. If the economy re-accelerates in the second half of 2026, we could see a return of “overheating” fears. In that scenario, bonds do not act as a hedge; they act as a source of volatility.

For the investor looking to insulate a portfolio against this “Anti-Goldilocks” scenario, two alternative defensive allocations merit serious consideration: Hard Assets and Digital Rails.

- Commodities: The “Anti-Bond”

If bonds can no longer be relied upon to dampen volatility, Commodities may be the logical successor for the role of portfolio diversifier. Historically, commodities are the only asset class that consistently performs well when bond yields are rising due to inflation or growth surprises. Given the “PTSD” supply constraints discussed earlier—where producers are refusing to add capacity despite rising demand—the structural case for the commodity complex (Copper, Energy, Uranium) is compelling. For allocators, moving from a “Paper Heavy” defense (Bonds) to a “Hard Asset” defense offers a way to hedge against the twin risks of fiscal largesse and physical scarcity.

- The Digital Collateral: Tokenization

Beyond atoms, there is a compelling case for the modernization of ownership itself. While many institutional investors remain skeptical of “Crypto” as a speculative asset class, a distinction should be made for “Tokenization” as a technological rail. The convergence of AI and Finance is creating a need for programmable value. Market research indicates that over $260 billion in Real World Assets (RWA)—from US Treasuries to private credit—have already moved on-chain. This isn’t about speculating on a meme coin; it’s about the efficiency of collateral. As AI agents begin to transact, they will likely bypass the friction of legacy banking rails in favor of tokenized settlement.

Investors might consider exposure to the infrastructure of this shift—not the casino, but the boring, industrial plumbing of the next financial system.

Conclusion: Solving the Equation

If 2025 was a “Very Good Year” defined by momentum, 2026 will be a “Worker’s Year” defined by selectivity.

The rising tide that lifted all boats is receding, revealing a landscape of stark dispersion. We have sectors priced for perfection (Hyperscalers) and sectors priced for disaster (Real Estate/Small Caps). We have a first half defined by political noise and a second half defined by economic clarity.

The “Two-Body” era was comfortable. It was easy to model. But the “493-Body Problem” is where the excess returns are hiding.

We are rotating capital. We are moving from the Cloud to the Edge. We are swapping our bond hedges for commodity hedges. And we are looking for the companies that have learned the hard lessons of the last decade and are choosing profit over ego. The investors caught in the “Binary Trap” will spend 2026 waiting for a Boom or a Bust that never arrives. We intend to spend it profitably in the middle.

IMPORTANT LEGAL DISCLOSURES

CURRENT MARKET DATA IS AS OF 12/31/2025. OPINIONS AND PREDICTIONS ARE AS OF 12/31/2025 AND ARE SUBJECT TO CHANGE AT ANY TIME BASED ON MARKET AND OTHER CONDITIONS. NO PREDICTIONS OR FORECASTS CAN BE GUARANTEED. INFORMATION CONTAINED HEREIN HAS BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE BUT IS NOT GUARANTEED.

THIS PRESENTATION (THE “PRESENTATION”) HAS BEEN PREPARED SOLELY FOR INFORMATION PURPOSES AND IS NOT INTENDED TO BE AN OFFER OR SOLICITATION AND IS BEING FURNISHED SOLELY FOR USE BY CLIENTS AND PROSPECTIVE CLIENTS IN CONSIDERING GFG CAPITAL, LLC (“GFG CAPITAL” OR THE “COMPANY”) AS THEIR INVESTMENT ADVISER. DO NOT USE THE FOREGOING AS THE SOLE BASIS OF INVESTMENT DECISIONS. ALL SOURCES DEEMED RELIABLE HOWEVER GFG CAPITAL ASSUMES NO RESPONSIBILITY FOR ANY INACCURACIES. THE OPINIONS CONTAINED HEREIN ARE NOT RECOMMENDATIONS.

THIS MATERIAL DOES NOT CONSTITUTE A RECOMMENDATION TO BUY OR SELL ANY SPECIFIC SECURITY, PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. INVESTING INVOLVES RISK, INCLUDING THE POSSIBLE LOSS OF A PRINCIPAL INVESTMENT.

INDEX PERFORMANCE IS PRESENTED FOR ILLUSTRATIVE PURPOSES ONLY. DIRECT INVESTMENT CANNOT BE MADE INTO AN INDEX. INVESTMENT IN EQUITIES INVOLVES MORE RISK THAN OTHER SECURITIES AND MAY HAVE THE POTENTIAL FOR HIGHER RETURNS AND GREATER LOSSES. BONDS HAVE INTEREST RATE RISK AND CREDIT RISK. AS INTEREST RATES RISE, EXISTING BOND PRICES FALL AND CAN CAUSE THE VALUE OF AN INVESTMENT TO DECLINE. CHANGES IN INTEREST RATES GENERALLY HAVE A GREATER EFFECT ON BONDS WITH LONGER MATURITIES THAN ON THOSE WITH SHORTER MATURITIES. CREDIT RISK REFERES TO THE POSSIBLITY THAT THE ISSUER OF THE BOND WILL NOT BE ABLE TO MAKE PRINCIPAL AND/OR INTEREST PAYMENTS.

THE INFORMATION CONTAINED HEREIN HAS BEEN PREPARED TO ASSIST INTERESTED PARTIES IN MAKING THEIR OWN EVALUATION OF GFG CAPITAL AND DOES NOT PURPORT TO CONTAIN ALL OF THE INFORMATION THAT A PROSPECTIVE CLIENT MAY DESIRE. IN ALL CASES, INTERESTED PARTIES SHOULD CONDUCT THEIR OWN INVESTIGATION AND ANALYSIS OF GFG CAPITAL AND THE DATA SET FORTH IN THIS PRESENTATION. FOR A FULL DESCRIPTION OF GFG CAPITAL’S ADVISORY SERVICES AND FEES, PLEASE REFER TO OUR FORM ADV PART 2 DISCLOSURE BROCHURE AVAILABLE BY REQUEST OR AT THE FOLLOWING WEBSITE: HTTP://WWW.ADVISERINFO.SEC.GOV/.

ALL COMMUNICATIONS, INQUIRIES AND REQUESTS FOR INFORMATION RELATING TO THIS PRESENTATION SHOULD BE ADDRESSED TO GFG CAPITAL AT 305-810-6500.